-

K线形态识别_空方尖兵

写在前面:

1. 本文中提到的“K线形态查看工具”的具体使用操作请查看该博文;

2. K线形体所处背景,诸如处在上升趋势、下降趋势、盘整等,背景内容在K线形态策略代码中没有体现;

3. 文中知识内容来自书籍《K线技术分析》by邱立波。目录

解说

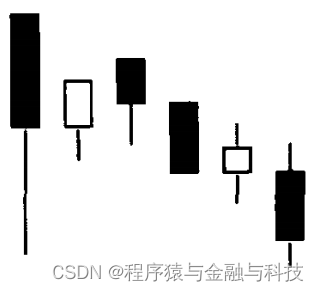

空方尖兵指出现在下跌行情中,由若干向下倾斜、收在第一根中阴线或大阴线长下影线下方的K线组成。

技术特征

1)出现在下跌行情中。

2)由若干K线组合而成。

3)在拉出一根中阴线或大阴线时,留下一根较长的下影线。

4)股价反弹后不久又跌至下影线的下方。

技术含义

空方尖兵是卖出信号,后市看跌。

第一根阴线的长下影线可以看做是空方大举进攻前向多方发动的一次试探性冲锋,如同深入敌方阵地的尖兵,所以称为空方尖兵。

空方尖兵表明多方的反击有心无力,时间短暂得如昙花一现,后市下跌的概率很大。交易者见到空方尖兵,应及时做空,离场观望。

K线形态策略代码

- def excute_strategy(daily_file_path):

- '''

- 名称:空方尖兵

- 识别:

- 1. 若干向下倾斜、收在第一根中阴线或大阴线长下影线下方的K线组合

- 自定义:

- 1. 长下影线 =》影线长度大于实体长度

- 2. 影线下方 =》实体中心点一下,影线最低点往上

- 3. 至少5根

- 前置条件:计算时间区间 2021-01-01 到 2022-01-01

- :param daily_file_path: 股票日数据文件路径

- :return:

- '''

- import pandas as pd

- import os

- start_date_str = '2013-01-01'

- end_date_str = '2014-01-01'

- df = pd.read_csv(daily_file_path,encoding='utf-8')

- # 删除停牌的数据

- df = df.loc[df['openPrice'] > 0].copy()

- df['o_date'] = df['tradeDate']

- df['o_date'] = pd.to_datetime(df['o_date'])

- df = df.loc[(df['o_date'] >= start_date_str) & (df['o_date']<=end_date_str)].copy()

- # 保存未复权收盘价数据

- df['close'] = df['closePrice']

- # 计算前复权数据

- df['openPrice'] = df['openPrice'] * df['accumAdjFactor']

- df['closePrice'] = df['closePrice'] * df['accumAdjFactor']

- df['highestPrice'] = df['highestPrice'] * df['accumAdjFactor']

- df['lowestPrice'] = df['lowestPrice'] * df['accumAdjFactor']

- # 开始计算

- df['type'] = 0

- df.loc[df['closePrice'] > df['openPrice'], 'type'] = 1

- df.loc[df['closePrice'] < df['openPrice'], 'type'] = -1

- df['body_length'] = abs(df['closePrice']-df['openPrice'])

- df['big_yeah'] = 0

- df.loc[(df['type']==-1) & (df['body_length']/df['closePrice'].shift(1)>0.02) & (df['closePrice']-df['lowestPrice']>df['body_length']),'big_yeah'] = 1

- df.reset_index(inplace=True)

- df.at[len(df)-1,'big_yeah'] = 1

- df['i_row'] = [i for i in range(len(df))]

- df_target = df.loc[df['big_yeah']==1].copy()

- target_list = df_target['i_row'].values.tolist()

- s_list = []

- e_list = []

- for i in range(len(target_list)-1):

- s_list.append(target_list[i])

- e_list.append(target_list[i+1])

- df['signal'] = 0

- df['signal_name'] = ''

- for s,e in zip(s_list,e_list):

- if e-s < 5:

- continue

- temp_e = None

- up_point = df.iloc[s]['closePrice'] + df.iloc[s]['body_length']*0.5

- down_point = df.iloc[s]['lowestPrice']

- for i in range(s+1,e):

- if df.iloc[i]['highestPrice']<=up_point and df.iloc[i]['lowestPrice']>=down_point:

- temp_e = i

- else:

- break

- if temp_e is None or temp_e-s < 5:

- continue

- df.loc[(df['i_row']>=s) & (df['i_row']<=temp_e),'signal'] = 1

- df.loc[(df['i_row']>=s) & (df['i_row']<=temp_e),'signal_name'] = str(temp_e-s)

- pass

- file_name = os.path.basename(daily_file_path)

- title_str = file_name.split('.')[0]

- line_data = {

- 'title_str':title_str,

- 'whole_header':['日期','收','开','高','低'],

- 'whole_df':df,

- 'whole_pd_header':['tradeDate','closePrice','openPrice','highestPrice','lowestPrice'],

- 'start_date_str':start_date_str,

- 'end_date_str':end_date_str,

- 'signal_type':'duration_detail',

- 'duration_len':[],

- 'temp':len(df.loc[df['signal']==1])

- }

- return line_data

结果

-

相关阅读:

使用 Python 进行 GUI 掷骰子模拟

【实战-08】flink DataStream 如何实现去重

java游戏制作-拼图游戏

人工智能证书的作用

SLAM从入门到精通(第一次hector slam建图)

选择排序、冒泡排序、插入排序【十大经典排序算法】

Nginx配置多个二级域名和CA证书的详细教程

详解HTTP协议版本(HTTP/1.0、1.1、2.0、3.0区别)

替换文章中的关键词

王学岗自定义ViewGroup在哪里获取控件

- 原文地址:https://blog.csdn.net/m0_37967652/article/details/127780099